Market Outlook

February 07, 2018

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are likely to open positive tracking global indices and SGX Nifty.

BSE Sensex

(1.6)

(561)

34,196

US stocks remain volatile over the course of the trading session before ending the

Nifty

(1.6)

(168)

10,498

day firmly in positive territory. The Dow Jones ended on upside front of 2.3% to

Mid Cap

(1.7)

(278)

16,281

close at 24,913 and the Nasdaq Composite edged up to 2.1%, to 7,116.

Small Cap

(2.2)

(390)

17,392

Bankex

(1.3)

(380)

29,197

U.K. shares fell sharply as a global market rout intensified and the second phase of

Brexit talks kicked off in London with the EU Chief Negotiator Michel Barnier

repeating his call for more ‘clarity' from the U.K. on its position. The FTSE 100 was

Global Indices

Chg (%)

(Pts)

(Close)

down by 2.6% to close at 7,141.

Dow Jones

2.3

567

24,913

Nasdaq

2.1

148

7,116

On domestic front, Indian shares opened sharply lower to extend their recent sell off

as growing concerns over fiscal slippages and the return of the long term capital

FTSE

(2.6)

(194)

7,141

gains tax on equities in this budget continued to haunt investors ahead of the RBI

Nikkei

3.1

660

22,271

policy. The Sensex ended on a downside front of 1.6% at 34,196 while the Nifty

Hang Seng

1.9

568

31,163

ended at 10,498 with a downside of 1.6%.

Shanghai Com

1.0

35

3,405

News Analysis

Advances / Declines

BSE

NSE

RBI likely to keep policy rates on hold

Advances

513

303

Detailed analysis on Pg2

Declines

2,271

1,540

Investor’s Ready Reckoner

Unchanged

143

38

Key Domestic & Global Indicators

Stock Watch: Latest investment recommendations on 150+ stocks

Volumes (` Cr)

Refer Pg5 onwards

BSE

5,349

NSE

39,339

Top Picks

CMP

Target

Upside

Company

Sector

Rating

(`)

(`)

(%)

Net Inflows (` Cr)

Net

Mtd

Ytd

Blue Star

Capital Goods

Buy

722

867

20.1

FII

(1,083)

1,372

14,356

Dewan Housing Finance

Financials

Buy

506

712

40.8

Asian Granito

Other

Buy

492

651

32.3

*MFs

(957)

(1,222)

6,165

Navkar Corporation

Other

Buy

168

265

57.8

KEI Industries

Capital Goods

Buy

352

436

23.9

Top Gainers

Price (`)

Chg (%)

More Top Picks on Pg4

Religare

43

5.0

Key Upcoming Events

Advenzymes

257

4.0

Previous

Consensus

Date

Region

Event Description

Vipind

351

3.9

Reading

Expectations

Bomdyeing

231

3.8

Feb07

India

RBI Reverse Repo rate

5.75

5.75

Feb07

India

RBI Cash Reserve ratio

4.00

4.00

Oil

349

3.7

Feb07

India

RBI Repo rate

6.00

6.00

Feb08

US

Initial Jobless claims

230.00

233.00

Top Losers

Price (`)

Chg (%)

Feb08

UK

Industrial Production (YoY)

2.50

0.30

More Events on Pg7

Vakrangee

213

(10.0)

Dbl

812

(8.2)

Pcjeweller

392

(7.5)

Ifci

23

(7.3)

Jpassociat

18

(7.1)

As on February 06 2018

Market Outlook

February 07, 2018

News Analysis

RBI likely to keep policy rates on hold

In the Reserve Bank of India's (RBI) Monetary Policy Committee (MPC) meeting,

which will be held in Mumbai, the apex bank is expected to keep policy rates on

hold for this week.

However, the bank may toughen its warning against inflation, lying on the ground

for a hike in 2018 after prices accelerated at the fastest pace in the last 17

months. The bank is also worried about high global crude prices.

Though RBI has held the rates steady since a 25 basis point cut in August 2017,

the prospects of rate hike have increased, as annual inflation accelerated to 5.21

percent in December 2017.

Economic and Political News

Decline in stock indices due to global market meltdown, not LTCG tax

Taxpayers' base is 80mn, no taxman can pick up a case on discretion

Centre sees its GST compensation to states at Rs 900 billion for FY19

RBI likely to keep policy rates on hold due to high inflation risks

Corporate News

Ashok Leyland to invest Rs 1 billion in electric vehicle technology

Airtel offers 2x data, add-on SIM with unlimited calls with postpaid plans

ICICI Securities gets Sebi's go-ahead for IPO to raise Rs 30bn-Rs 40bn

Israel to give 750,000euros to AI for launching Delhi-Tel Aviv flight

Market Outlook

February 07, 2018

Quarterly Bloomberg Brokers Consensus Estimate

Cipla Ltd - Feb 07, 2018

Particulars ( ` cr)

3QFY18E

3QFY17

y-o-y (%)

2QFY18

q-o-q (%)

Sales

4,115

3,647

12.8

4,082

0.8

EBIDTA

835

677

23.4

804

3.8

%

20.3

18.5

19.7

PAT

460

374

22.9

434

5.9

Aurobindo Pharma Ltd. - Feb 07, 2018

Particulars ( ` cr)

3QFY18E

3QFY17

y-o-y (%)

2QFY18

q-o-q (%)

Sales

4,255

2,521

68.7

3,073

38.4

EBIDTA

1,012

634

59.6

1,039

(2.6)

%

23.8

25.2

33.8

PAT

663

441

50.3

752

(11.8)

Eicher Motors Ltd. - Feb 07, 2018

Particulars ( ` cr)

3QFY18E

3QFY17

y-o-y (%)

2QFY18

q-o-q (%)

Sales

2,221

1,834

21.1

2,167

2.5

EBIDTA

704

577

22.1

682

3.2

%

31.7

31.5

31.5

PAT

538

418

28.7

518

3.8

Market Outlook

February 07, 2018

Top Picks

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

Strong growth in domestic business due to its leade`hip

in acute therapeutic segment. Alkem expects to launch

Alkem Laboratories

25,910

2,167

2,441

12.6

more products in USA, which bodes for its international

business.

We expect the company would report strong profitability

Asian Granito

1,481

492

651

32.3

owing to better product mix, higher B2C sales and

amalgamation synergy.

Favorable outlook for the AC industry to augur well for

Cooling products business which is out pacing the

Blue Star

6,926

722

867

20.1

market growth. EMPPAC division's profitability to

improve once operating environment turns around.

With a focus on the low and medium income (LMI)

consumer segment, the company has increased its

Dewan Housing Finance

15,857

506

712

40.8

presence in tier-II & III cities where the growth

opportunity is immense.

Loan growth is likely to pick up after a sluggish FY17.

Lower credit cost will help in strong bottom-line growth.

Karur Vysya Bank

8,024

110

160

44.9

Increasing share of CASA will help in NIM

improvement.

High order book execution in EPC segment, rising B2C

KEI Industries

2,757

352

436

23.9

sales and higher exports to boost the revenues and

profitability

Expected to benefit from the lower capex requirement

Music Broadcast

2,009

352

475

34.9

and 15 year long radio broadcast licensing.

Massive capacity expansion along with rail advantage

Navkar Corporation

2,527

168

265

57.8

at ICD as well CFS augur well for the company

Strong brands and distribution network would boost

Siyaram Silk Mills

2,974

635

851

34.1

growth going ahead. Stock currently trades at an

inexpensive valuation.

Market leadership in Hindi news genre and no.

2

viewership ranking in English news genre, exit from the

TV Today Network

2,596

435

500

14.9

radio business, and anticipated growth in ad spends by

corporate to benefit the stock.

After GST, the company is expected to see higher

volumes along with improving product mix. The Gujarat

Maruti Suzuki

2,71,402

8,984

10,619

18.2

plant will also enable higher operating leverage which

will be margin accretive.

We expect loan book to grow at 24.3% over next two

GIC Housing

2,094

389

655

68.4

year; change in borrowing mix will help in NIM

improvement

We expect CPIL to report net Revenue/PAT CAGR of

~17%/16% over FY2017-20E mainly due to healthy

6,665

300

400

33.3

growth in plywood & lamination business, forayed into

Century Plyboards India

MDF & Particle boards on back of strong brand &

distribution network.

We expect sales/PAT to grow at 13.5%/20% over next

LT Foods

2,763

86

128

48.1

two years on the back of strong distribution network &

addition of new products in portfolio.

We expect sales/PAT to grow at 13%/16% over next two

years on the back of strong healthy demand in writing

Ruchira Papers

374

167

244

46.1

& printing paper and Kraft paper. Further, China had

banned making paper from waste pulp which would

benefit Indian paper companies.

We expect financialisation of savings and increasing

Aditya Birla Capital

36942

158

230

45.5

penetration in Insurance & Mutual fund would ensure

steady growth.

Source: Company, Angel Research

Market Outlook

February 07, 2018

Fundamental Call

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

CCL is likely to maintain the strong growth trajectory

CCL Products

3,884

292

360

23.3

over FY18-20 backed by capacity expansion and new

geographical foray

We forecast Nilkamal to report top-line CAGR of ~9%

to `2,635cr over FY17-20E on the back of healthy

Nilkamal

2,453

1,644

2,178

32.5

demand growth in plastic division. On the bottom-line

front, we estimate ~10% CAGR to `162cr owing to

improvement in volumes.

We expect sales/PAT to grow at 9%/14% over next two

years on the back of healthy demand growth in

Shreyans Industries

234

169

247

46.2

printing. Further, China had banned making paper

from waste pulp which would benefit Indian paper

companies.

The prism has diversified exposure in the different

segment such as Cement, Tile & ready mix concrete.

Prism Cement

6,133

122

160

31.3

Thus we believe, PCL is in the right place to capture

ongoing government spending on affordable housing

and infrastructure projects.

Source: Company, Angel Research

Market Outlook

February 07, 2018

Key Upcoming Events

Result Calendar

Date

Company

February 07, 2018

FAG Bearings, Areva, BGR Energy , Hexaware, Indraprasth Gas, Elecon Engineering, Cipla, Aurobindo Pharma

February 08, 2018

Bharat Forge, BHEL, ABB, ACC, Reliance Capital, Andhra Bank, SAIL, Petronet LNG, GSPL, Page Industries

Source: Bloomberg, Angel Research

Global economic events release calendar

Bloomberg Data

Date

Time

Country

Event Description

Unit

Period

Last Reported

Estimated

Feb 07, 2018

2:30 PMIndia

RBI Reverse Repo rate

%

Feb 7

5.75

5.75

2:30 PMIndia

RBI Cash Reserve ratio

%

Feb 7

4.00

4.00

2:30 PMIndia

RBI Repo rate

%

Feb 7

6.00

6.00

Feb 08, 2018

7:00 PMUS

Initial Jobless claims

Thousands

Feb 3

230.00

233.00

3:00 PMUK

Industrial Production (YoY)

% Change

Dec

2.50

0.30

China

Exports YoY%

% Change

Jan

10.90

10.80

Feb 09, 2018

5:30 PMUK

BOE Announces rates

% Ratio

Feb 8

0.50

0.50

7:00 AMChina

Consumer Price Index (YoY)

% Change

Jan

1.80

1.50

Feb 12, 2018

5:30 PMIndia

Industrial Production YoY

% Change

Dec

8.40

Feb 13, 2018

3:00 PMUK

CPI (YoY)

% Change

Jan

3.00

Feb 14, 2018

3:30 PMEuro Zone Euro-Zone GDP s.a. (QoQ)

% Change

4Q P

0.60

12:00 PMIndia

Monthly Wholesale Prices YoY%

% Change

Jan

3.58

7:00 PMUS

Consumer price index (mom)

% Change

Jan

0.10

0.30

12:30 PMGermany GDP nsa (YoY)

% Change

4Q P

2.30

Feb 15, 2018

7:45 PMUS

Industrial Production

%

Jan

0.89

0.30

Source: Bloomberg, Angel Research

Market Outlook

February 07, 2018

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

10.0

9.0

8.4

9.1

9.0

8.0

8.0

7.9

7.0

7.6

7.5

8.0

7.3

7.2

7.0

6.0

4.8

7.0

6.3

5.0

4.4

4.1

6.1

6.1

5.7

3.5

3.2

6.0

4.0

2.9

3.0

2.0

5.0

2.0

1.2

1.0

4.0

1.0

-

3.0

(1.0)

(0.3)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

56.0

Mfg. PMI

Services PMI

(%)

6.0

54.0

5.2

4.9

52.0

5.0

3.9

50.0

3.7

3.6

4.0

3.3

3.3

3.2

3.0

48.0

3.0

2.4

2.2

46.0

2.0

1.5

44.0

1.0

42.0

40.0

-

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

60.0

6.50

50.0

6.00

40.0

5.50

30.0

5.00

20.0

4.50

10.0

4.00

0.0

3.50

(10.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

Market Outlook

February 07, 2018

Global watch

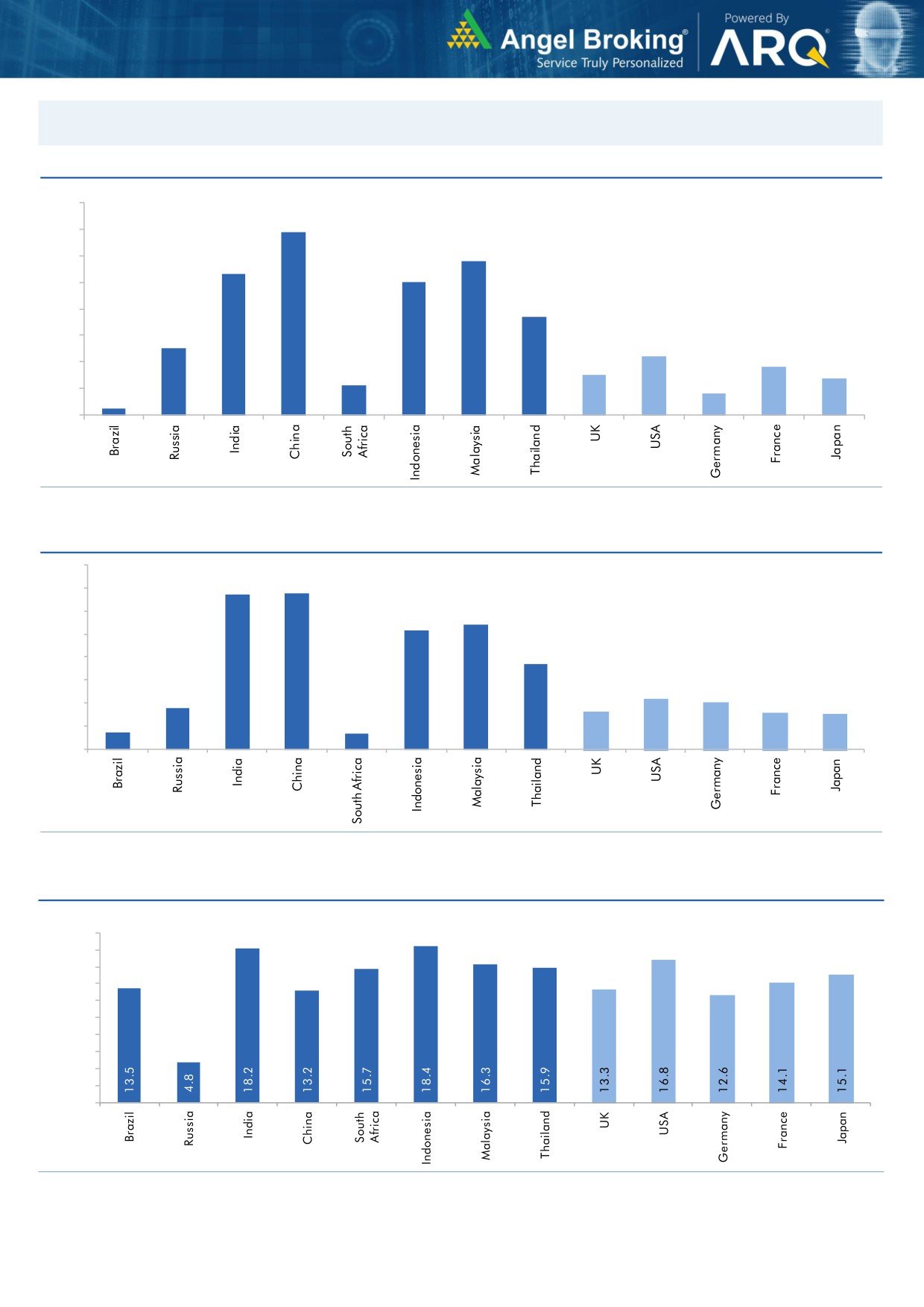

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.9

7.0

5.8

6.0

5.3

5.0

5.0

1.1

3.7

4.0

2.5

3.0

2.2

1.8

2.0

1.5

1.4

0.8

1.0

0.3

-

Source: Bloomberg, Angel Research

Exhibit 2: 2017 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

6.7

6.8

7.0

6.0

5.4

5.2

5.0

3.7

4.0

3.0

1.8

2.2

2.0

1.7

1.6

2.0

0.7

1.5

0.7

1.0

-

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

February 07, 2018

Exhibit 4: Relative performance of indices across globe

Returns (%)

Country

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

83,894

6.7

12.2

30.5

Russia

Micex

2,238

1.8

8.0

1.3

India

Nifty

10,498

(0.1)

0.4

20.2

China

Shanghai Composite

3,371

(0.1)

(0.3)

7.9

South Africa

Top 40

49,856

(5.7)

(6.3)

9.8

Mexico

Mexbol

49,305

(0.9)

1.4

4.4

Indonesia

LQ45

1,090

2.1

10.3

26.7

Malaysia

KLCI

1,812

1.1

3.9

7.6

Thailand

SET 50

1,162

(0.5)

7.6

16.6

USA

Dow Jones

24,913

(0.6)

5.9

24.0

UK

FTSE

7,141

(7.5)

(5.5)

(0.7)

Japan

Nikkei

21,610

(8.1)

(1.8)

13.5

Germany

DAX

12,393

(7.0)

(8.1)

7.3

France

CAC

5,162

(5.6)

(6.5)

6.9

Source: Bloomberg, Angel Research p68in4

Market Outlook

February 07, 2018

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India

Limited,Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.